Recent reports have highlighted concerns about the UK’s gas supply, driven by a combination of factors. Colder-than-average temperatures have significantly increased heating demand, while low renewable generation has placed greater reliance on gas-fired power. These challenges are compounded by reduced gas storage levels, which currently stand at 67%. With the UK undersupplied on some days, storage withdrawals and LNG imports have become vital to meeting demand. These conditions underscore the importance of maintaining resilient energy systems during peak winter months.

Despite this, the UK government and National Gas, the country’s largest gas network operator, remain confident in the nation’s ability to meet winter energy demands. This confidence is bolstered by robust LNG imports and diverse supply routes, with UK LNG injection rates increasing by 25-30% compared to 2023.

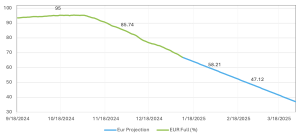

Storage levels, while lower than in 2023 and 2024, are projected to close March 25 with 36% remaining if current storage withdrawal rates sustain, surpassing levels recorded in 2021 and 2022. Additionally, Europe is making significant strides in expanding LNG infrastructure, with plans to boost import capacity by 42% by 2026. Floating storage regasification units (FSRUs) in Italy, Poland, and Greece are expected to become operational by Spring 2025, further enhancing regional energy security.

While LNG remains a critical component of the UK’s energy supply, market participants can remain assured that flows are unlikely to drop to zero during 2025. However, these challenges emphasise the need for ongoing investment in storage capacity and diverse energy sources to support a resilient energy future.