Why Now Could Be the Right Time to Review Your Long-Term Energy Strategy

July 9, 2026

Climate Change Agreements (CCAs): Are You Making the Most of Your Energy Cost Savings?

July 15, 2026

UK Energy Market Summary to Friday 10th July 2026

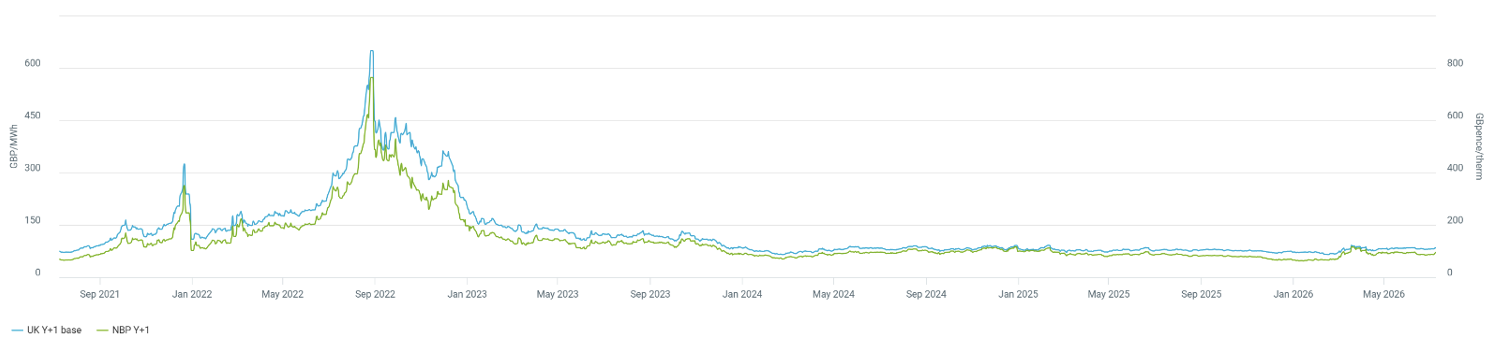

Closing prices 10.07.2026

Wholesale gas and power markets strengthened during the week ending 10th July as renewed geopolitical tensions in the Middle East added a fresh risk premium across European energy markets. UK NBP and European TTF gas prices moved higher following attacks on commercial shipping near the Strait of Hormuz, raising concerns over global LNG supply security whilst Europe remains heavily reliant on imported LNG to replenish gas storage ahead of winter.

Despite the stronger price environment, European gas storage continued to build steadily throughout the week, providing some reassurance over winter security of supply. However, inventories remain below both last year’s levels and the five-year seasonal average, leaving wholesale gas prices sensitive to any disruption in LNG imports, Norwegian supply or prolonged periods of higher summer demand.

Prompt UK and European electricity markets also remained firm, supported by periods of warm weather, weaker wind generation and increased reliance on gas-fired power stations to balance the system.

Curve UK Gas & Electricity Markets

Other Energy Markets

Brent crude oil rose sharply during the week, closing at approximately $76/bbl after renewed military escalation involving Iran reintroduced a geopolitical risk premium into global oil markets. Although OPEC+ confirmed a further increase in production from August, concerns surrounding shipping through the Strait of Hormuz and the potential impact on global oil and LNG flows remained the dominant influence on market sentiment.

Looking ahead, wholesale energy markets are expected to remain focused on geopolitical developments in the Middle East, European gas storage injections, global LNG availability and summer weather patterns. Whilst near-term volatility has increased, the forward curve remains backwardated, with longer-dated gas and electricity contracts continuing to offer attractive value for organisations seeking to secure future energy costs and improve long-term budget certainty.